Page 139 - DMGT104_FINANCIAL_ACCOUNTING

P. 139

Unit 7: Trial Balance

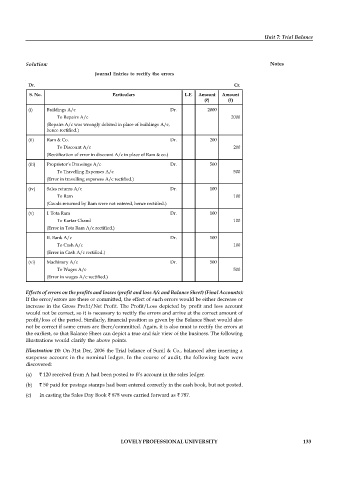

Solution: Notes

Journal Entries to rectify the errors

Dr. Cr.

S. No. Particulars L.F. Amount Amount

( ) ( )

(i) Buildings A/c Dr. 2000

To Repairs A/c 2000

(Repairs A/c was wrongly debited in place of buildings A/c,

hence rectified.)

(ii) Ram & Co. Dr. 200

To Discount A/c 200

(Rectification of error in discount A/c in place of Ram & co.)

(iii) Proprietor’s Drawings A/c Dr. 500

To Travelling Expenses A/c 500

(Error in travelling expenses A/c rectified.)

(iv) Sales returns A/c Dr. 100

To Ram 100

(Goods returned by Ram were not entered, hence rectified.)

(v) I. Tota Ram Dr. 100

To Kartar Chand 100

(Error in Tota Ram A/c rectified.)

II. Bank A/c Dr. 100

To Cash A/c 100

(Error in Cash A/c rectified.)

(vi) Machinery A/c Dr. 500

To Wages A/c 500

(Error in wages A/c rectified.)

Effects of errors on the profits and losses (profit and loss A/c and Balance Sheet) (Final Accounts):

If the error/errors are there or committed, the effect of such errors would be either decrease or

increase in the Gross Profit/Net Profit. The Profit/Loss depicted by profit and loss account

would not be correct, so it is necessary to rectify the errors and arrive at the correct amount of

profit/loss of the period. Similarly, financial position as given by the Balance Sheet would also

not be correct if some errors are there/committed. Again, it is also must to rectify the errors at

the earliest, so that Balance Sheet can depict a true and fair view of the business. The following

illustrations would clarify the above points.

Illustration 10: On 31st Dec, 2006 the Trial balance of Sunil & Co., balanced after inserting a

suspense account in the nominal ledger. In the course of audit, the following facts were

discovered:

(a) 120 received from A had been posted to B’s account in the sales ledger.

(b) 50 paid for postage stamps had been entered correctly in the cash book, but not posted.

(c) In casting the Sales Day Book 878 were carried forward as 787.

LOVELY PROFESSIONAL UNIVERSITY 133