Page 136 - DMGT104_FINANCIAL_ACCOUNTING

P. 136

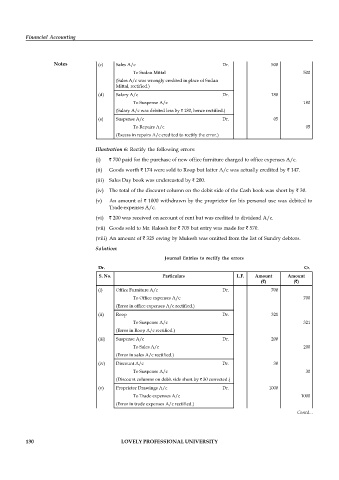

Dr. Cr.

S. No. Particulars L.F. Amount Amount

( ) ( )

Financial Accounting

(b) Suspense A/c Dr. 200

To Rent A/c 200

(Rent A/c was wrongly debited, hence rectified by 200.)

Notes (c) Sales A/c Dr. 500

To Sudan Mittal 500

(Sales A/c was wrongly credited in place of Sudan

Mittal, rectified.)

(d) Salary A/c Dr. 180

To Suspense A/c 180

(Salary A/c was debited less by 180, hence rectified.)

(e) Suspense A/c Dr. 05

To Repairs A/c 05

(Excess in repairs A/c credited to rectify the error.)

Illustration 6: Rectify the following errors:

(i) 700 paid for the purchase of new office furniture charged to office expenses A/c.

(ii) Goods worth 174 were sold to Roop but latter A/c was actually credited by 147.

(iii) Sales Day book was undercasted by 200.

(iv) The total of the discount column on the debit side of the Cash book was short by 30.

(v) An amount of 1000 withdrawn by the proprietor for his personal use was debited to

Trade expenses A/c.

(vi) 200 was received on account of rent but was credited to dividend A/c.

(vii) Goods sold to Mr. Rakesh for 705 but entry was made for 570.

(viii) An amount of 325 owing by Mukesh was omitted from the list of Sundry debtors.

Solution:

Journal Entries to rectify the errors

Dr. Cr.

S. No. Particulars L.F. Amount Amount

( ) ( )

(i) Office Furniture A/c Dr. 700

To Office expenses A/c 700

(Error in office expenses A/c rectified.)

(ii) Roop Dr. 321

To Suspense A/c 321

(Error in Roop A/c rectified.)

(iii) Suspense A/c Dr. 200

To Sales A/c 200

(Error in sales A/c rectified.)

(iv) Discount A/c Dr. 30

To Suspense A/c 30

(Discount columns on debit side short by 30 corrected.)

(v) Proprietor Drawings A/c Dr. 1000

To Trade expenses A/c 1000

(Error in trade expenses A/c rectified.)

(vi) Dividend A/c Dr. 200 Contd.. .

To Rent A/c 200

(Error in dividend A/c rectified.)

(vii) Rakesh Dr. 135

130 LOVELY PROFESSIONAL UNIVERSITY

To Sales A/c 135

(Error in Rakesh and Sales A/c rectified [ 705 – 570].)

(viii) Mukesh (Sundry Debtors) Dr. 325

To Suspense A/c 325

(Error in Mukesh A/c rectified.)