Page 142 - DMGT104_FINANCIAL_ACCOUNTING

P. 142

Financial Accounting

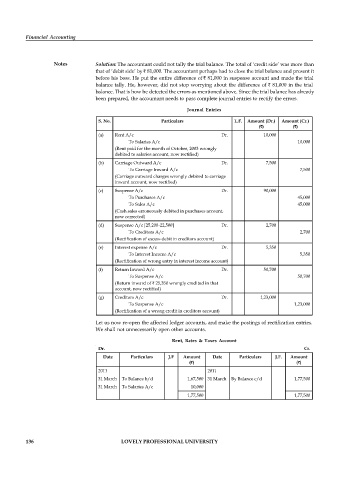

Notes Solution: The accountant could not tally the trial balance. The total of ‘credit side’ was more than

that of ‘debit side’ by 81,000. The accountant perhaps had to close the trial balance and present it

before his boss. He put the entire difference of 81,000 in suspense account and made the trial

balance tally. He, however, did not stop worrying about the difference of 81,000 in the trial

balance. That is how he detected the errors as mentioned above. Since the trial balance has already

been prepared, the accountant needs to pass complete journal entries to rectify the errors.

Journal Entries

S. No. Particulars L.F. Amount (Dr.) Amount (Cr.)

( ) ( )

(a) Rent A/c Dr. 10,000

To Salaries A/c 10,000

(Rent paid for the month of October, 2003 wrongly

debited to salaries account, now rectified)

(b) Carriage Outward A/c Dr. 7,500

To Carriage Inward A/c 7,500

(Carriage outward charges wrongly debited to carriage

inward account, now rectified)

(c) Suspense A/c Dr. 90,000

To Purchases A/c 45,000

To Sales A/c 45,000

(Cash sales erroneously debited in purchases account,

now corrected)

(d) Suspense A/c [25,200-22,500] Dr. 2,700

To Creditors A/c 2,700

(Rectification of excess debit in creditors account)

(e) Interest expense A/c Dr. 5,350

To Interest Income A/c 5,350

(Rectification of wrong entry in interest income account)

(f) Return Inward A/c Dr. 50,700

To Suspense A/c 50,700

(Return inward of 25,350 wrongly credited in that

account, now rectified)

(g) Creditors A/c Dr. 1,23,000

To Suspense A/c 1,23,000

(Rectification of a wrong credit in creditors account)

Let us now re-open the affected ledger accounts, and make the postings of rectification entries.

We shall not unnecessarily open other accounts.

Rent, Rates & Taxes Account

Dr. Cr.

Date Particulars J.F Amount Date Particulars J.F. Amount

( ) ( )

2011 2011

31 March To Balance b/d 1,67,500 31 March By Balance c/d 1,77,500

31 March To Salaries A/c 10,000

1,77,500 1,77,500

136 LOVELY PROFESSIONAL UNIVERSITY