Page 210 - DMGT104_FINANCIAL_ACCOUNTING

P. 210

( )

( )

Raw materials: 2007 2006

46,000.00

42,000.00

Opening Stock

Purchases 4,74,000.00 4,30,000.00

5,20,000.00 4,72,000.00

Less: Closing Stock 52,000.00 46,000.00

Financial Accounting Add: Material Consumed 4,68,000.00 4,26,000.00

Direct Labour 6,32,000.00 5,06,000.00

Manufacturing Expenses 2,84,000.00 2,42,000.00

13,84,000.00 11,74,000.00

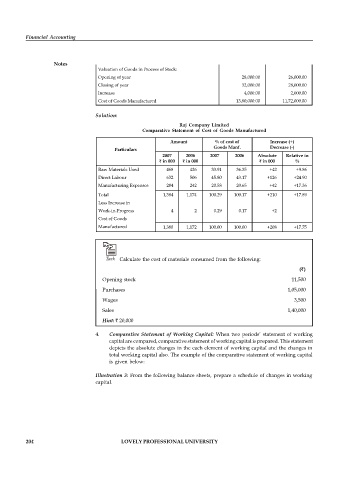

Notes

Valuation of Goods in Process of Stock:

Opening of year 28,000.00 26,000.00

Closing of year 32,000.00 28,000.00

Increase 4,000.00 2,000.00

Cost of Goods Manufactured 13,80,000.00 11,72,000.00

Solution:

Raj Company Limited

Comparative Statement of Cost of Goods Manufactured

Amount % of cost of Increase (+)

Goods Manf. Decrease (-)

Particulars

2007 2006 2007 2006 Absolute Relative in

in 000 in 000 in 000 %

Raw Materials Used 468 426 33.91 36.35 +42 +9.86

Direct Labour 632 506 45.80 43.17 +126 +24.90

Manufacturing Expenses 284 242 20.58 20.65 +42 +17.36

Total 1,384 1,174 100.29 100.17 +210 +17.89

Less Increase in

Work-in-Progress 4 2 0.29 0.17 +2

Cost of Goods

Manufactured 1,380 1,172 100.00 100.00 +208 +17.75

Task Calculate the cost of materials consumed from the following:

( )

Opening stock 11,500

Purchases 1,05,000

Wages 3,500

Sales 1,40,000

Hint: 20,000

4. Comparative Statement of Working Capital: When two periods’ statement of working

capital are compared, comparative statement of working capital is prepared. This statement

depicts the absolute changes in the each element of working capital and the changes in

total working capital also. The example of the comparative statement of working capital

is given below:

Illustration 3: From the following balance sheets, prepare a schedule of changes in working

capital.

204 LOVELY PROFESSIONAL UNIVERSITY