Page 211 - DMGT104_FINANCIAL_ACCOUNTING

P. 211

Unit 9: Analysis and Interpretation of Financial Statements

Notes

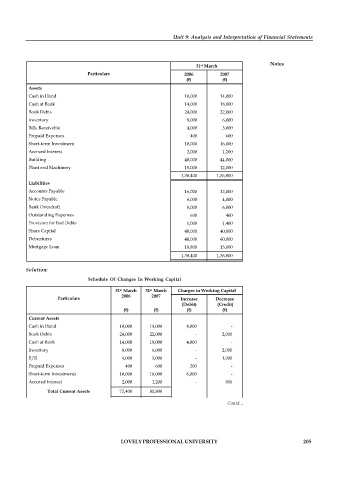

31 st March

Particulars 2006 2007

( ) ( )

Assets

Cash in Hand 10,000 14,000

Cash at Bank 14,000 18,000

Book Debts 24,000 22,000

Inventory 8,000 6,000

Bills Receivable 4,000 3,000

Prepaid Expenses 400 600

Short-term Investment 10,000 16,000

Accrued Interest 2,000 1,200

Building 40,000 44,000

Plant and Machinery 18,000 12,000

1,30,400 1,36,800

Liabilities

Accounts Payable 16,000 12,000

Notes Payable 6,000 4,000

Bank Overdraft 8,000 6,000

Outstanding Expenses 600 400

Provision for Bad Debts 1,000 1,400

Share Capital 40,000 40,000

Debentures 40,000 60,000

Mortgage Loan 18,800 13,000

1,30,400 1,36,800

Solution:

Schedule Of Changes In Working Capital

31 st March 31 st March Charges in Working Capital

2006 2007

Particulars Increase Decrease

(Debit) (Credit)

( ) ( ) ( ) ( )

Current Assets

Cash in Hand 10,000 14,000 4,000 -

Book Debts 24,000 22,000 - 2,000

Cash at Bank 14,000 18,000 4,000 -

Inventory 8,000 6,000 - 2,000

B/R 4,000 3,000 - 1,000

Prepaid Expenses 400 600 200 -

Short-term Investments 10,000 16,000 6,000 -

Accured Interest 2,000 1,200 - 800

Total Current Assets 72,400 80,800

Current Liabilities

Contd...

Account Payable 16,000 12,000 4,000 -

Notes Payable 6,000 4,000 2,000 -

Bank Overdraft 8,000 6,000 2,000 -

Outstanding Expenses 600 400 200 -

1,000

1,400

-

Provision for Bed Debts LOVELY PROFESSIONAL UNIVERSITY 400 205

Total of Current Liabilities 31,600 23,800

Working Capital

(Current Assets – Current Liabilities) 40,800 57,000 - 16,200

Net Increase in Working Capital 16,200 - - -

57,000 57,000 22,400 22,400