Page 218 - DMGT202_COST_AND_MANAGEMENT_ACCOUNTING

P. 218

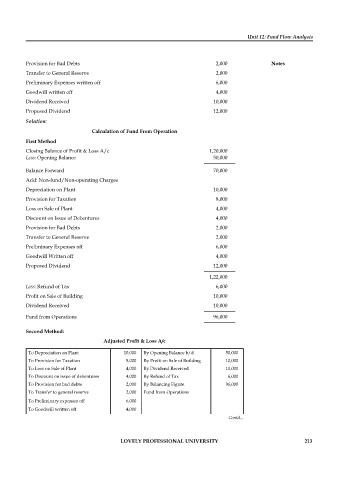

Unit 12: Fund Flow Analysis

Provision for Bad Debts 2,000 Notes

Transfer to General Reserve 2,000

Preliminary Expenses written off 6,000

Goodwill written off 4,000

Dividend Received 10,000

Proposed Dividend 12,000

Solution:

Calculation of Fund From Operation

First Method

Closing Balance of Profit & Loss A/c 1,20,000

Less: Opening Balance 50,000

Balance Forward 70,000

Add: Non-fund/Non-operating Charges

Depreciation on Plant 10,000

Provision for Taxation 8,000

Loss on Sale of Plant 4,000

Discount on Issue of Debentures 4,000

Provision for Bad Debts 2,000

Transfer to General Reserve 2,000

Preliminary Expenses off 6,000

Goodwill Written off 4,000

Proposed Dividend 12,000

1,22,000

Less: Refund of Tax 6,000

Profit on Sale of Building 10,000

Dividend Received 10,000

Fund from Operations 96,000

Second Method:

Adjusted Profit & Loss A/c

To Depreciation on Plant 10,000 By Opening Balance b/d 50,000

To Provision for Taxation 8,000 By Profit on Sale of Building 10,000

To Loss on Sale of Plant 4,000 By Dividend Received 10,000

To Discount on issue of debentures 4,000 By Refund of Tax 6,000

To Provision for bad debts 2,000 By Balancing Figure 96,000

To Transfer to general reserve 2,000 Fund from Operations

To Preliminary expenses off 6,000

To Goodwill written off 4,000

Contd...

LOVELY PROFESSIONAL UNIVERSITY 213