Page 149 - DMGT403_ACCOUNTING_FOR_MANAGERS

P. 149

Accounting for Managers

Notes 7.3 Steps in the Preparation of Fund Flow Statement

1. First and foremost step is to prepare the statement of changes in working capital i.e. to

identify the flow of fund/movement of fund through the detection of changes in the

volume of working capital.

2. Second step is the preparation of Non-current A/c items-Changes in the volume of

Non-current A/cs have to be prepared only in order to quantify the flow fund i.e. either

sources or application of fund.

3. Third step is the preparation Adjusted Profit & Loss A/c, which already elaborately

discussed in the early part of the unit.

4. Last step is the preparation of fund flow statement.

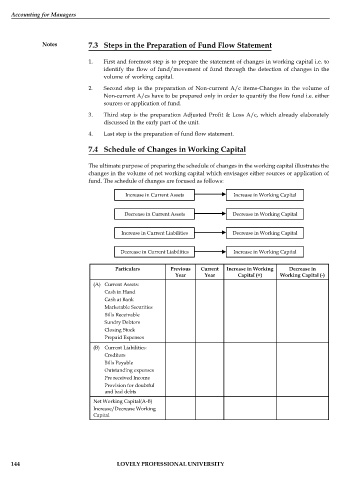

7.4 Schedule of Changes in Working Capital

The ultimate purpose of preparing the schedule of changes in the working capital illustrates the

changes in the volume of net working capital which envisages either sources or application of

fund. The schedule of changes are focused as follows:

Increase in Current Assets Increase in Working Capital

Decrease in Current Assets Decrease in Working Capital

Increase in Current Liabilities Decrease in Working Capital

Decrease in Current Liabilities Increase in Working Capital

Particulars Previous Current Increase in Working Decrease in

Year Year Capital (+) Working Capital (-)

(A) Current Assets:

Cash in Hand

Cash at Bank

Marketable Securities

Bills Receivable

Sundry Debtors

Closing Stock

Prepaid Expenses

(B) Current Liabilities:

Creditors

Bills Payable

Outstanding expenses

Pre received Income

Provision for doubtful

and bad debts

Net Working Capital(A-B)

Increase/Decrease Working

Capital

144 LOVELY PROFESSIONAL UNIVERSITY