Page 198 - DMGT403_ACCOUNTING_FOR_MANAGERS

P. 198

Estimated Sales Rs. 80,000 Rs. 1,00,000

Level Level

Unit 9: Budgetary Control

Fixed Overhead

Advertisement on Radio 2,000 2,000

Advertisement on TV 12,000 12,000

Salary to Sales Admin. Staff 20,000 20,000 Notes

Salary to Sales force 15,000 15,000

Expenses of the sales dept – Rent 5,000 5,000

Total Sales Fixed Overhead (A) 54,000 54,000

Variable Overhead

Salesmen’s Commission 2% 1,440 10,290

Agents’ Commission 6.5% 520 682.5

Carriage outward 5% 4,000 5,000

Total Variable Overhead (B) 5,960 5682.5

Total Sales overhead(A+B) 59,960 59682.5

Cash Budget

Cash budget is nothing but an estimation of cash receipts and cash payments for specified

period. It is prepared by the head of the accounts department i.e. chief accounts officer.

The utility of the cash budget is as follows:

1. To meet the revenue and capital expenditures with adequate funds.

2. It should highlight the additional requirement cash whenever the need arises.

3. Keeping of excessive funds available in the business firm would not fetch any return to the

enterprise but this estimate of future cash needs and resources will guide the firm to plan

for an effective investment out of the surplus funds estimated; enhances the wealth of the

investors through proper investment planning out of the future funds available.

Cash budget can be prepared in three different ways:

1. Receipts and payments method

2. Adjusted profit and loss account

3. Balance Sheet Method

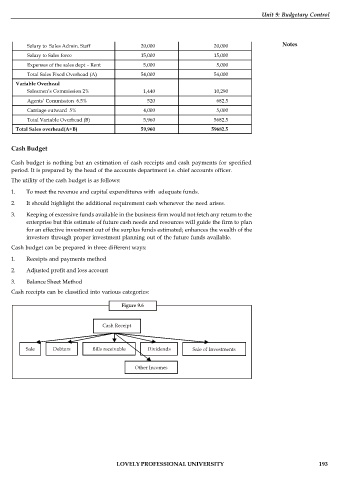

Cash receipts can be classified into various categories:

Figure 9.6

Cash Receipt

Sale Debtors Bills receivable Dividends Sale of Investments

Other Incomes

LOVELY PROFESSIONAL UNIVERSITY 193