Page 259 - DECO401_MICROECONOMIC_THEORY_ENGLISH

P. 259

Microeconomic Theory

Notes production of the monopolist is OM units. Average Cost Curve (AC) touches Average Revenue Curve

(AR) at point A at this level production is at point A, Price OP (AR) of the product is equal to average

cost AM (AC) so the monopolist will earn only Normal Profits at equilibrium production because at

equilibrium quantity and average cost are equal to price (Average Income) (AC = AR).

(3) Minimum Loss: In short run, demand of the goods decreases due to depression and as a result prices

fall the monopolist will continue to produce at this reduced price if he is getting Average variable cost

(AVC) at this price. If the monopolist will have to determine the prices less than the average variable cost

then he will stop the production. Therefore, the monopolist in the short run may have to bear minimum

loss means can bear loss of average fixed cost. In equilibrium situation prices (AR) of the product is

equal to Average variable cost (AVC) so the monopolist may have to bear average fixed cost loss. This

loss has to bear by monopolist even at the time when he stops work during short run. Therefore.,

Minimum Loss = AC – AVC = AFC

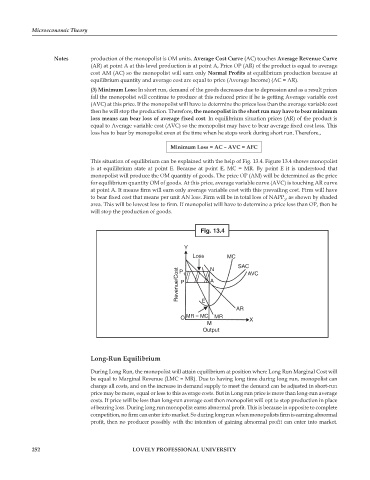

This situation of equilibrium can be explained with the help of Fig. 13.4. Figure 13.4 shows monopolist

is at equilibrium state at point E. Because at point E, MC = MR. By point E it is understood that

monopolist will produce the OM quantity of goods. The price OP (AM) will be determined as the price

for equilibrium quantity OM of goods. At this price, average variable curve (AVC) is touching AR curve

at point A. It means firm will earn only average variable cost with this prevailing cost. Firm will have

to bear fixed cost that means per unit AN loss. Firm will be in total loss of NAPP , as shown by shaded

1

area. This will be lowest loss to firm. If monopolist will have to determine a price less than OP, then he

will stop the production of goods.

Fig. 13.4

Y

Loss MC

SAC AVC

Revenue/Cost P A

N

P

1

E

AR

O MR = MC MR X

M

Output

Long-Run Equilibrium

During Long Run, the monopolist will attain equilibrium at position where Long Run Marginal Cost will

be equal to Marginal Revenue (LMC = MR). Due to having long time during long run, monopolist can

change all costs, and on the increase in demand supply to meet the demand can be adjusted in short-run

price may be more, equal or less to this average costs. But in Long run price is more than long-run average

costs. If price will be less than long-run average cost then monopolist will opt to stop production in place

of bearing loss. During long run monopolist earns abnormal profit. This is because in opposite to complete

competition, no firm can enter into market. So during long run when monopolists firm is earning abnormal

profit, then no producer possibly with the intention of gaining abnormal profit can enter into market.

252 LOVELY PROFESSIONAL UNIVERSITY