Page 176 - DCOM202_COST_ACCOUNTING_I

P. 176

Cost Accounting – I

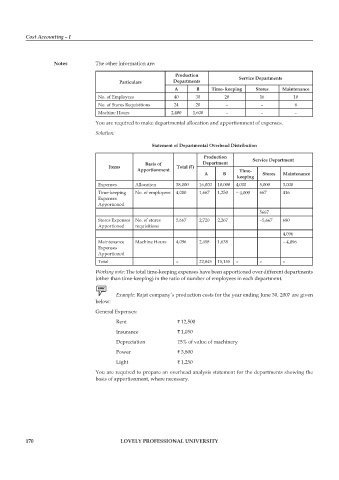

Notes The other information are:

Production Service departments

Particulars departments

A B Time- keeping Stores Maintenance

No. of Employees 40 30 20 16 10

No. of Stores Requisitions 24 20 – – 6

Machine Hours 2,400 1,600 – – –

You are required to make departmental allocation and apportionment of expenses.

Solution:

Statement of departmental Overhead distribution

Production Service department

Basis of department

Items Total (`)

Apportionment Time-

A B Stores Maintenance

keeping

Expenses Allocation 38,000 16,000 10,000 4,000 5,000 3,000

Time-keeping No. of employees 4,000 1,667 1,250 − 4,000 667 416

Expenses

Apportioned

5667

Stores Expenses No. of stores 5,667 2,720 2,267 −5,667 680

Apportioned requisitions

4,096

Maintenance Machine Hours 4,096 2,458 1,638 − 4,096

Expenses

Apportioned

Total – 22,845 15,155 – – –

Working note: The total time-keeping expenses have been apportioned over different departments

(other than time-keeping) in the ratio of number of employees in each department.

Example: Rajat company’s production costs for the year ending June 30, 2007 are given

below:

General Expenses:

Rent ` 12,500

Insurance ` 1,050

Depreciation 15% of value of machinery

power ` 3,800

Light ` 1,250

You are required to prepare an overhead analysis statement for the departments showing the

basis of apportionment, where necessary.

170 LOVELY PROFESSIONAL UNIVERSITY