Page 182 - DCOM202_COST_ACCOUNTING_I

P. 182

Cost Accounting – I

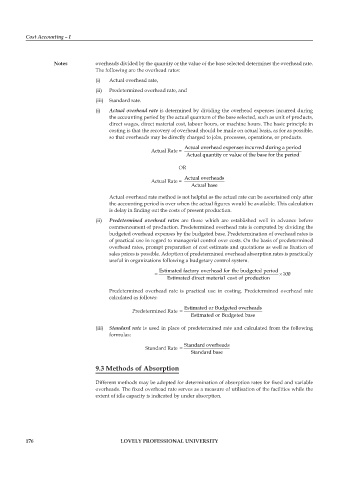

Notes overheads divided by the quantity or the value of the base selected determines the overhead rate.

The following are the overhead rates:

(i) Actual overhead rate,

(ii) predetermined overhead rate, and

(iii) Standard rate.

(i) Actual overhead rate is determined by dividing the overhead expenses incurred during

the accounting period by the actual quantum of the base selected, such as unit of products,

direct wages, direct material cost, labour hours, or machine hours. The basic principle in

costing is that the recovery of overhead should be made on actual basis, as for as possible,

so that overheads may be directly charged to jobs, processes, operations, or products.

Actual overhead expenses incurred during a period

Actual Rate =

Actual quaantity or value of the base for the period

OR

Actual overheads

Actual Rate =

Actual base

Actual overhead rate method is not helpful as the actual rate can be ascertained only after

the accounting period is over when the actual figures would be available. This calculation

is delay in finding out the costs of present production.

(ii) Predetermined overhead rates are those which are established well in advance before

commencement of production. predetermined overhead rate is computed by dividing the

budgeted overhead expenses by the budgeted base. predetermination of overhead rates is

of practical use in regard to managerial control over costs. On the basis of predetermined

overhead rates, prompt preparation of cost estimate and quotations as well as fixation of

sales prices is possible. Adoption of predetermined overhead absorption rates is practically

useful in organizations following a budgetary control system.

Estimatedfactory overhead forthe budgeted period

= ×100

Estimated direct material cos tofproduction

e

predetermined overhead rate is practical use in costing. predetermined overhead rate

calculated as follows:

EstimatedorBudgetedoverheads

predetermined Rate =

EstimatedorBudgetedbase

(iii) Standard rate is used in place of predetermined rate and calculated from the following

formulas:

Standard overheads

Standard Rate =

Standard base

9.3 Methods of Absorption

Different methods may be adopted for determination of absorption rates for fixed and variable

overheads. The fixed overhead rate serves as a measure of utilisation of the facilities while the

extent of idle capacity is indicated by under absorption.

176 LOVELY PROFESSIONAL UNIVERSITY