Page 269 - DCOM202_COST_ACCOUNTING_I

P. 269

Unit 13: Normal Wastage, Abnormal Loss and Abnormal Gain

Notes

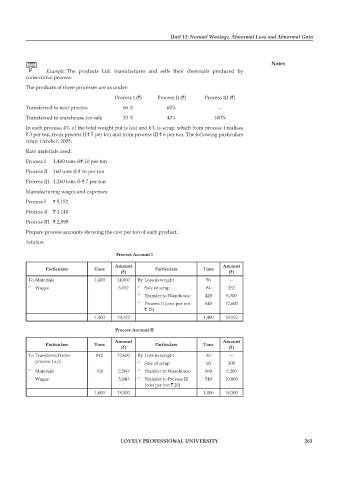

Example: The products Ltd. manufactures and sells their chemicals produced by

consecutive process:

The products of three processes are as under:

process I (`) process II (`) process III (`)

Transferred to next process 66 % 60% —

Transferred to warehouse for sale 33 % 40% 100%

In each process, 4% of the total weight put is lost and 6% is scrap, which from process I realises

` 3 per ton, from process II ` 5 per ton and from process III ` 6 per ton. The following particulars

relate October, 2005:

Raw materials used:

process I 1,400 tons @` 10 per ton

process II 160 tons @ ` 16 per ton

process III 1,260 tons @ ` 7 per ton

Manufacturing wages and expenses:

process I ` 5,152

process II ` 3,140

process III ` 2,895

prepare process accounts showing the cost per ton of each product.

Solution:

Process Account I

Amount Amount

Particulars Tons Particulars Tons

(`) (`)

To Materials 1,400 14,000 By Loss in weight 56 --

“ Wages 5,152 “ Sale of scrap 84 252

“ Transfer to Warehouse 420 6,300

“ Process II (cost per ton 840 12,600

` 15)

1,400 19,152 1,400 19,152

Process Account II

Amount Amount

Particulars Tons Particulars Tons

(`) (`)

To Transferred from 840 12,600 By Loss in weight 40 --

process I a/c “ Sale of scrap 60 300

“ Materials 160 2,560 “ Transfer to Warehouse 360 7,200

“ Wages 3,140 “ Transfer to Process III 540 10,800

(cost per ton ` 20)

1,000 18,300 1,000 18,300

LOVELY PROFESSIONAL UNIVERSITY 263