Page 125 - DCOM206_COST_ACCOUNTING_II

P. 125

Cost Accounting – II

Notes (x) Estimated amount of operating expenses on the basis of credit terms, agreement and

timing of disbursement,

(xi) Minimum cash balance desired depending upon business needs and market conditions,

and

(xii) Hire purchase and instalment sale agreement relating to instalment payments for purchase.

6.5.1 Role of Cash Budget

Efficient cash management through relevant and timely cash budgets may help:

(i) Provide funds for normal growth,

(ii) Secure optimum working capital needed for smooth and unhindered running of the

operation and planning for payments to shareholders,

(iii) Facilitate temporary investment of cash whenever, and to whatever extent, found in excess,

and

(iv) Ease strains of a cash shortage.

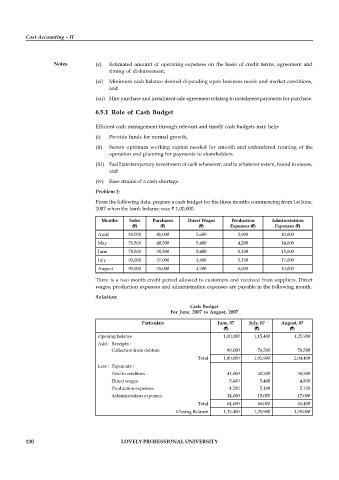

Problem 1:

From the following data, prepare a cash budget for the three months commencing from 1st June,

2007 when the bank balance was ` 1,00,000.

Months Sales Purchases Direct Wages Production Administration

(`) (`) (`) Expenses (`) Expenses (`)

April 80,000 41,000 5,600 3,900 10,000

May 76,500 40,500 5,400 4,200 14,000

June 78,500 38,500 5,400 5,100 15,000

July 90,000 37,000 4,800 5,100 17,000

August 95,000 35,000 4,700 6,000 13,000

There is a two month credit period allowed to customers and received from suppliers. Direct

wages, production expenses and administration expenses are payable in the following month.

Solution:

Cash Budget

For June, 2007 to August, 2007

Particulars June, 07 July, 07 August, 07

(`) (`) (`)

Opening balance 1,00,000 1,15,400 1,25,900

Add : Receipts :

Collection from debtors 80,000 76,500 78,500

Total 1,80,000 1,91,900 2,04,400

Less : Payments :

Paid to creditors 41,000 40,500 38,500

Direct wages 5,400 5,400 4,800

Production expenses 4,200 5,100 5,100

Administration expenses 14,000 15,000 17,000

Total 64,600 66,000 65,400

Closing Balance 1,15,400 1,25,900 1,39,000

120 LOVELY PROFESSIONAL UNIVERSITY