Page 217 - DCOM205_ACCOUNTING_FOR_COMPANIES_II

P. 217

Accounting for Companies – II

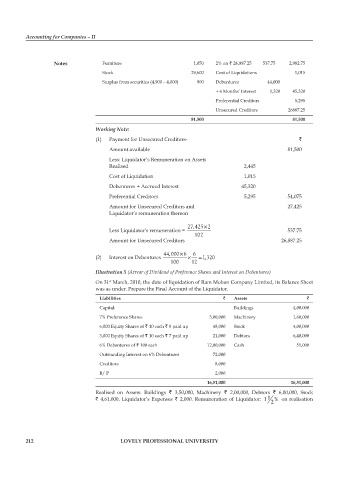

notes Furniture 1,050 2% on ` 26,887.25 537.75 2,982.75

Stock 29,600 Cost of Liquidations 1,015

Surplus from securities (4,900 – 4,000) 900 Debentures 44,000

+ 6 Months’ Interest 1,320 45,320

Preferential Creditors 5,295

Unsecured Creditors 26887.25

81,500 81,500

Working Note:

(1) Payment for Unsecured Creditors- `

Amount available 81,500

Less: Liquidator’s Remuneration on Assets

Realised 2,445

Cost of Liquidation 1,015

Debentures + Accrued Interest 45,320

Preferential Creditors 5,295 54,075

Amount for Unsecured Creditors and 27,425

Liquidator’s remuneration thereon

27,425 ×2

Less Liquidator’s remuneration = 537.75

102

Amount for Unsecured Creditors 26,887.25

44,000 ×6 6

(2) Interest on Debentures × = 1,320

100 12

Illustration 5 (Arrear of Dividend of Preference Shares and Interest on Debentures)

On 31 March, 2010, the date of liquidation of Ram Mohan Company Limited, its Balance Sheet

st

was as under. Prepare the Final Account of the Liquidator.

liabilities ` assets `

Capital: Buildings 4,00,000

7% Preference Shares 3,00,000 Machinery 1,60,000

6,000 Equity Shares of ` 10 each ` 8 paid up 48,000 Stock 4,00,000

3,000 Equity Shares of ` 10 each ` 7 paid up 21,000 Debtors 6,40,000

6% Debentures of ` 100 each 12,00,000 Cash 51,000

Outstanding Interest on 6% Debentures 72,000

Creditors 8,000

B/ P 2,000

16,51,000 16,51,000

Realised on Assets: Buildings ` 3,50,000, Machinery ` 2,00,000, Debtors ` 6,00,000, Stock

` 4,61,000, Liquidator’s Expenses ` 2,000. Remuneration of Liquidator: 1 1 2 % on realisation

212 lovely professional university