Page 227 - DCOM205_ACCOUNTING_FOR_COMPANIES_II

P. 227

Accounting for Companies – II

notes

Notes As there is a legal preference of the receiver for costs and remuneration and

preferential creditors over the payment of debenture-holders, they are paid off first.

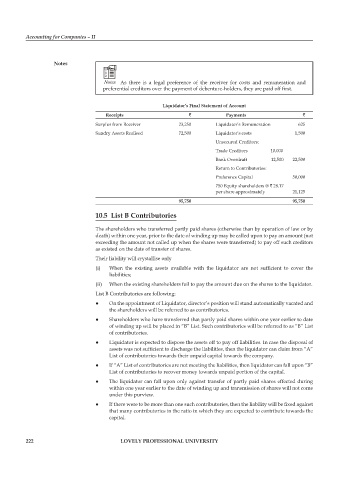

liquidator’s final statement of account

receipts ` payments `

Surplus from Receiver 23,250 Liquidator’s Remuneration 625

Sundry Assets Realised 72,500 Liquidator’s costs 1,500

Unsecured Creditors:

Trade Creditors 10,000

Bank Overdraft 12,500 22,500

Return to Contributories:

Preference Capital 50,000

750 Equity shareholders @ ` 28.17

per share approximately 21,125

95,750 95,750

10.5 list B contributories

The shareholders who transferred partly paid shares (otherwise than by operation of law or by

death) within one year, prior to the date of winding up may be called upon to pay an amount (not

exceeding the amount not called up when the shares were transferred) to pay off such creditors

as existed on the date of transfer of shares.

Their liability will crystallise only

(i) When the existing assets available with the liquidator are not sufficient to cover the

liabilities;

(ii) When the existing shareholders fail to pay the amount due on the shares to the liquidator.

List B Contributories are following:

l z On the appointment of Liquidator, director’s position will stand automatically vacated and

the shareholders will be referred to as contributories.

l z Shareholders who have transferred that partly paid shares within one year earlier to date

of winding up will be placed in “B” List. Such contributories will be referred to as “B” List

of contributories.

l z Liquidator is expected to dispose the assets off to pay off liabilities. In case the disposal of

assets was not sufficient to discharge the liabilities, then the liquidator can claim from “A”

List of contributories towards their unpaid capital towards the company.

l z If “A” List of contributories are not meeting the liabilities, then liquidator can fall upon “B”

List of contributories to recover money towards unpaid portion of the capital.

l z The liquidator can fall upon only against transfer of partly paid shares effected during

within one year earlier to the date of winding up and transmission of shares will not come

under this purview.

l z If there were to be more than one such contributories, then the liability will be fixed against

that many contributories in the ratio in which they are expected to contribute towards the

capital.

222 lovely professional university