Page 121 - DMGT514_MANAGEMENT_CONTROL_SYSTEMS

P. 121

Management Control Systems

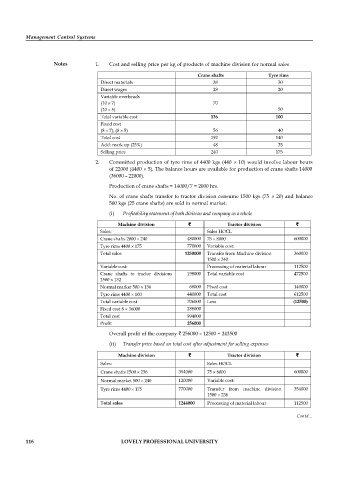

Notes 1. Cost and selling price per kg of products of machine division for normal sales

Crane shafts Tyre rims

Direct materials 38 30

Direct wages 28 20

Variable overheads

(10 7) 70

(10 5) 50

Total variable cost 136 100

Fixed cost

(8 7), (8 5) 56 40

Total cost 192 140

Add: mark up (25%) 48 35

Selling price 240 175

2. Committed production of tyre rims of 4400 kgs (440 10) would involve labour hours

of 22000 (4400 5). The balance hours are available for production of crane shafts 14000

(36000 – 22000).

Production of crane shafts = 14000/7 = 2000 hrs.

No. of crane shafts transfer to tractor division consume 1500 kgs (75 20) and balance

500 kgs (25 crane shafts) are sold in normal market.

(i) Profitability statement of both division and company as a whole

Machine division ` Tractor division `

Sales: Sales HOCL

Crane shafts 2000 240 480000 75 8000 600000

Tyre rims 4400 175 770000 Variable cost:

Total sales 1250000 Transfer from Machine division 360000

1500 240

Variable cost: Processing of material labour 112500

Crane shafts to tractor divisions 198000 Total variable cost 472500

1500 132

Normal market 500 136 68000 Fixed cost 140000

Tyre rims 4400 100 440000 Total cost 612500

Total variable cost 706000 Loss (12500)

Fixed cost 8 36000 288000

Total cost 994000

Profit 256000

Overall profit of the company ` 256000 – 12500 = 243500

(ii) Transfer price based on total cost after adjustment for selling expenses

Machine division ` Tractor division `

Sales: Sales HOCL

Crane shafts 1500 236 354000 75 8000 600000

Normal market 500 240 120000 Variable cost:

Tyre rims 4400 175 770000 Transfer from machine division 354000

1500 236

Total sales 1244000 Processing of material labour 112500

Variable cost: Total variable cost 466500

Contd...

Crane shafts to tractor divisions

1500*132 198000 Fixed cost 140000

Normal market 500 136 68000 Total cost 606500

116 LOVELY PROFESSIONAL UNIVERSITY

Tyre rims 4400 100 440000 Loss (6500)

Total variable cost 706000

Fixed cost 8 36000 288000

Total cost 994000

Profit 250000