Page 292 - DCOM202_COST_ACCOUNTING_I

P. 292

Cost Accounting – I

Notes closing work-in-progress and thus the closing work-in-progress appears cost of opening

work-in-progress. The completed units are at their current cost.

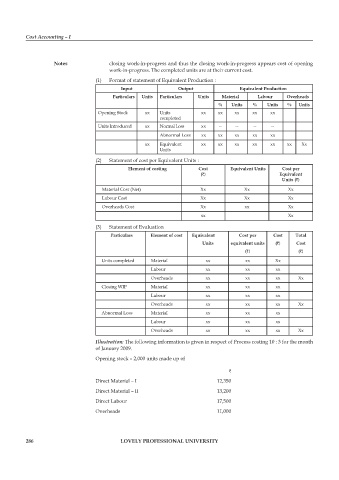

(1) Format of statement of Equivalent production :

Input Output Equivalent Production

Particulars Units Particulars Units Material Labour Overheads

% Units % Units % Units

Opening Stock xx Units xx xx xx xx xx

completed

Units Introduced xx Normal Loss xx -- -- -- --

Abnormal Loss xx xx xx xx xx

xx Equivalent xx xx xx xx xx xx Xx

Units

(2) Statement of cost per Equivalent Units :

Element of costing Cost Equivalent Units Cost per

(`) Equivalent

Units (`)

Material Cost (Net) Xx Xx Xx

Labour Cost Xx Xx Xx

Overheads Cost Xx xx Xx

xx Xx

(3) Statement of Evaluation

Particulars Element of cost Equivalent Cost per Cost Total

Units equivalent units (`) Cost

(`) (`)

Units completed Material xx xx Xx

Labour xx xx xx

Overheads xx xx xx Xx

Closing WIp Material xx xx xx

Labour xx xx xx

Overheads xx xx xx Xx

Abnormal Loss Material xx xx xx

Labour xx xx xx

Overheads xx xx xx Xx

Illustration: The following information is given in respect of process costing 10 : 3 for the month

of January 2009.

Opening stock – 2,000 units made up of

`

Direct Material – I 12,350

Direct Material – II 13,200

Direct Labour 17,500

Overheads 11,000

286 LOVELY PROFESSIONAL UNIVERSITY