Page 123 - DCOM205_ACCOUNTING_FOR_COMPANIES_II

P. 123

Accounting for Companies – II

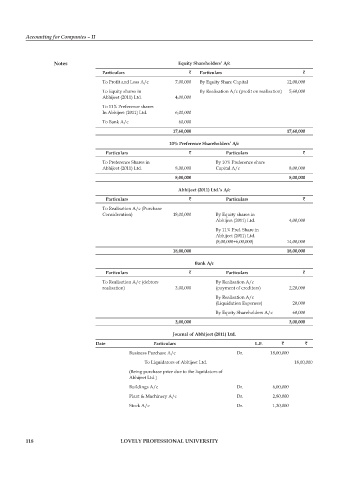

notes equity shareholders’ a/c

particulars ` particulars `

To Profit and Loss A/c 7,00,000 By Equity Share Capital 12,00,000

To Equity shares in By Realisation A/c (profit on realisation) 5,60,000

Abhijeet (2011) Ltd. 4,00,000

To 11% Preference shares

In Abhijeet (2011) Ltd. 6,00,000

To Bank A/c 60,000

17,60,000 17,60,000

10% preference shareholders’ a/c

particulars ` particulars `

To Preference Shares in By 10% Preference share

Abhijeet (2011) Ltd. 8,00,000 Capital A/c 8,00,000

8,00,000 8,00,000

abhijeet (2011) ltd.’s a/c

particulars ` particulars `

To Realisation A/c (Purchase

Consideration) 18,00,000 By Equity shares in

Abhijeet (2011) Ltd. 4,00,000

By 11% Pref. Share in

Abhijeet (2011) Ltd.

(8,00,000+6,00,000) 14,00,000

18,00,000 18,00,000

Bank a/c

particulars ` particulars `

To Realisation A/c (debtors By Realisation A/c

realisation) 3,00,000 (payment of creditors) 2,20,000

By Realisation A/c

(Liquidation Expenses) 20,000

By Equity Shareholders A/c 60,000

3,00,000 3,00,000

Journal of abhijeet (2011) ltd.

Date particulars l.f. ` `

Business Purchase A/c Dr. 18,00,000

To Liquidators of Abhijeet Ltd. 18,00,000

(Being purchase price due to the liquidators of

Abhijeet Ltd.)

Buildings A/c Dr. 6,00,000

Plant & Machinery A/c Dr. 2,80,000

Stock A/c Dr. 1,20,000

118 lovely professional university