Page 194 - DMGT514_MANAGEMENT_CONTROL_SYSTEMS

P. 194

Unit 9: Performance Measurement Systems

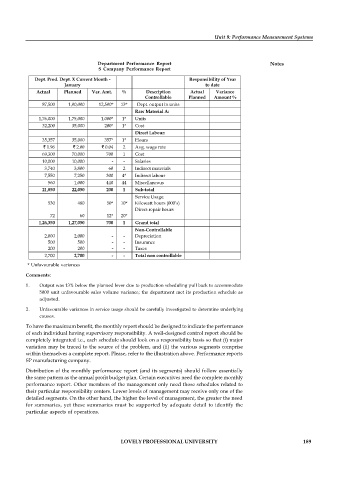

Department Performance Report Notes

S Company Performance Report

Dept. Prod. Dept. X Current Month - Responsibility of Year

January to date

Actual Planned Var. Amt. % Description Actual Variance

Controllable Planned Amount %

87,500 1,00,000 12,500* 13* Dept. output in units

Raw Material A:

1,76,000 1,75,000 1,000* 1* Units

32,200 35,000 200* 1* Cost

Direct Labour:

35,357 35,000 357* 1* Hours

` 1.96 ` 2.00 ` 0.04 2 Avg. wage rate

69,300 70,000 700 1 Cost

10,000 10,000 - - Salaries

3,740 3,800 60 2 Indirect materials

7,550 7,250 300 4* Indirect labour

560 1,000 440 44 Miscellaneous

21,850 22,050 200 1 Sub-total

Service Usage:

530 480 50* 10* Kilowatt hours (000’s)

Direct repair hours

72 60 12* 20*

1,26,350 1,27,050 700 1 Grand total

Non-Controllable

2,000 2,000 - - Depreciation

500 500 - - Insurance

200 200 - - Taxes

2,700 2,700 - - Total non controllable

* Unfavourable variances

Comments:

1. Output was 13% below the planned lever due to production scheduling pull back to accommodate

5000 unit unfavourable sales volume variance; the department met its production schedule as

adjusted.

2. Unfavourable variances in service usage should be carefully investigated to determine underlying

causes.

To have the maximum benefit, the monthly report should be designed to indicate the performance

of each individual having supervisory responsibility. A well-designed control report should be

completely integrated i.e., each schedule should look on a responsibility basis so that (i) major

variation may be traced to the source of the problem, and (ii) the various segments comprise

within themselves a complete report. Please, refer to the illustration above. Performance reports

SP manufacturing company.

Distribution of the monthly performance report (and its segments) should follow essentially

the same pattern as the annual profit budget plan. Certain executives need the complete monthly

performance report. Other members of the management only need those schedules related to

their particular responsibility centers. Lower levels of management may receive only one of the

detailed segments. On the other hand, the higher the level of management, the greater the need

for summaries, yet these summaries must be supported by adequate detail to identify the

particular aspects of operations.

LOVELY PROFESSIONAL UNIVERSITY 189