Page 252 - DCOM205_ACCOUNTING_FOR_COMPANIES_II

P. 252

Unit 11: Valuation of Goodwill

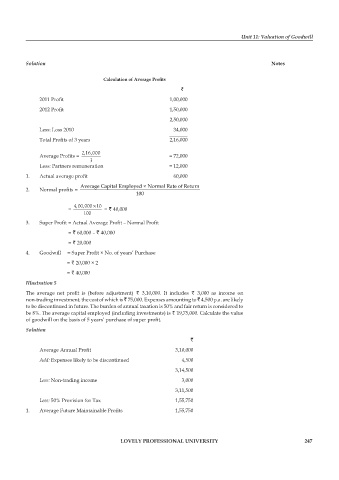

Solution notes

Calculation of Average Profits

`

2011 Profit 1,00,000

2012 Profit 1,50,000

2,50,000

Less: Loss 2010 34,000

Total Profits of 3 years 2,16,000

Average Profits = 2,16,000 = 72,000

3

Less: Partners remuneration = 12,000

1. Actual average profit 60,000

Average Capital Employed × Normal Rate of Return

2. Normal profits =

100

×

= 4,00,000 10 = ` 40,000

100

3. Super Profit = Actual Average Profit – Normal Profit

= ` 60,000 – ` 40,000

= ` 20,000

4. Goodwill = Super Profit × No. of years’ Purchase

= ` 20,000 × 2

= ` 40,000

Illustration 5

The average net profit is (before adjustment) ` 3,10,000. It includes ` 3,000 as income on

non-trading investment, the cost of which is ` 75,000. Expenses amounting to ` 4,500 p.a. are likely

to be discontinued in future. The burden of annual taxation is 50% and fair return is considered to

be 8%. The average capital employed (including investments) is ` 19,75,000. Calculate the value

of goodwill on the basis of 5 years’ purchase of super profit.

Solution

`

Average Annual Profit 3,10,000

Add: Expenses likely to be discontinued 4,500

3,14,500

Less: Non-trading income 3,000

3,11,500

Less: 50% Provision for Tax 1,55,750

1. Average Future Maintainable Profits 1,55,750

lovely professional university 247